Ignore Trump At Your Own Risk

Worst Policy Mistake in 100 Years?

TL; DR

Trump just tripled tariffs on Mexico and the EU—and markets are still partying.

Inflation is ticking up: core CPI rose to 2.9% and more tariff-driven price spikes are coming.

The Fed’s September rate cut odds just fell to 52%. Ignore this at your own risk.

Following a one-time inflation spike, tariffs could then take us into a recession

In short, we could be setting up for a perfect storm that could hit the economy in 2026, or even earlier.

Ignore Trump at Your Own Risk

Stocks keep rallying as if nothing happened.

That’s baffling because something huge happened:

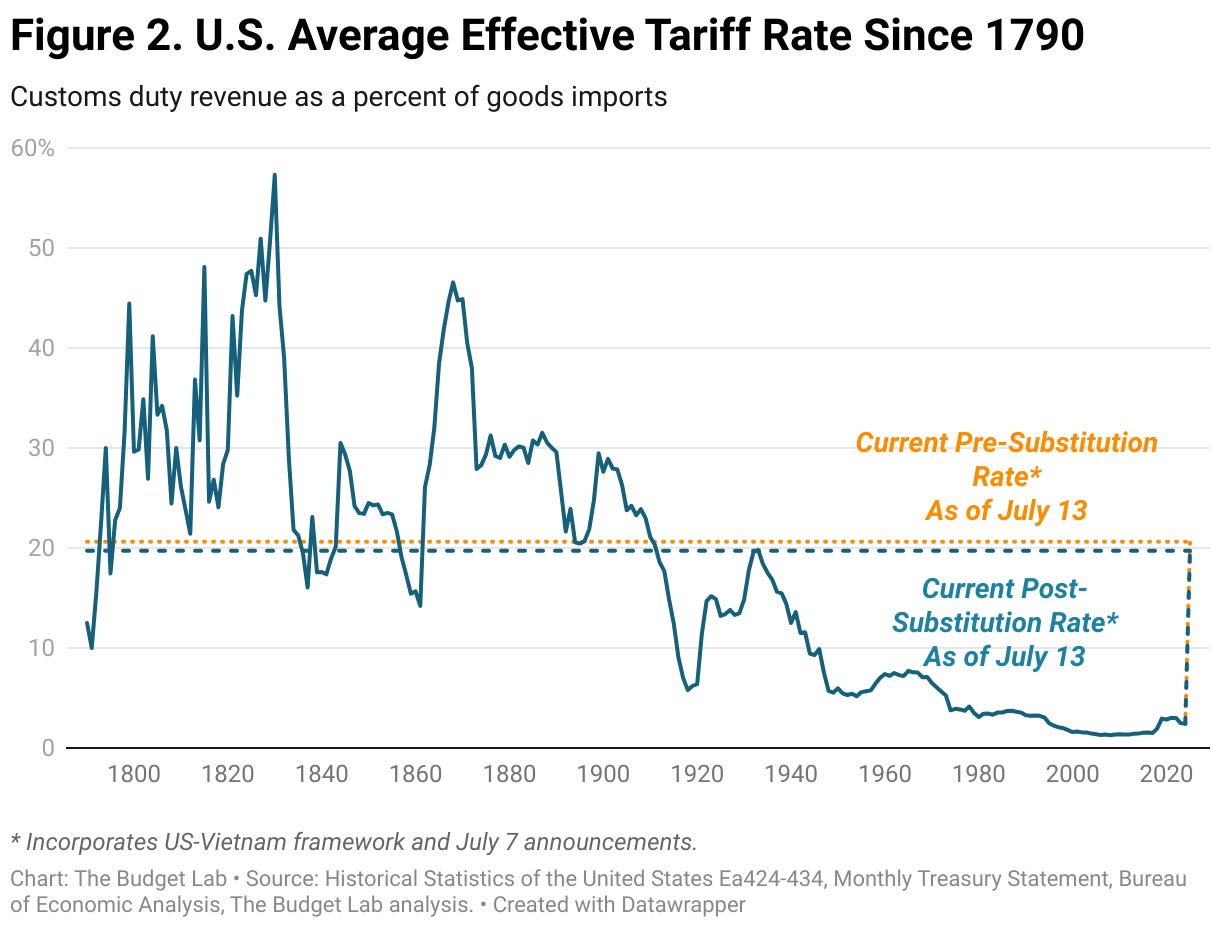

Trump has unleashed the biggest tariff escalation in decades. The baseline tariff of 10% will triple to 30% on Mexico and the EU starting August 1, while imports from most other nations will face blanket rates of 15-20%. On top of that, he’s floated 50% tariffs on copper, plus threats on pharmaceuticals and semiconductors.

And yet, markets yawned. Why? Because investors have been conditioned to assume Trump is bluffing. He’s threatened before and backed down. But that bet looks dangerous now.

Why This Time Is Different

Two things have changed:

Trump thinks tariffs work. His own words: “I think tariffs have been very well received. The stock market hit a new all-time high today.” Market resilience is convincing him tariffs have no cost.

His ego is on the line. The perception that he “always chickens out” before deadlines makes follow-through more likely this time. If markets stay complacent, he has every reason to prove them wrong.

And the issue here is a double whammy of a one-time inflation hit, followed by a recesiinary hit to the economy

Inflation Is Already Creeping Back

For months, the narrative was simple: “Tariffs don’t matter. Inflation is dead. The Fed can cut.” The latest CPI report blew that up.

Headline CPI jumped from 2.4% to 2.7% in June.

Core CPI climbed from 2.8% to 2.9%, reversing disinflation trends.

Tariff-sensitive goods surged:

Apparel: +0.4%

Footwear: +0.7%

Appliances: Biggest jump in 5 years

Toys: Largest spike since 2021

And this is just the first wave. New tariffs hitting in August won’t fully filter into prices until fall. Copper, pharma, and chips could keep inflation elevated well into 2026.

First Inflation, Then Deflation

It’s not that hard to understand. Do tariffs cause inflation or deflation? I say both

We will initially see a one-time hit to prices as tariffs are digested and companies try to push out the cost to consumers.

However, in the long run, a tariff is simply a tax on the economy. Money is being siphonned off from consumers and or corporations and into the government. June alone saw $27 billion in tariff revenue flow into government coffers.

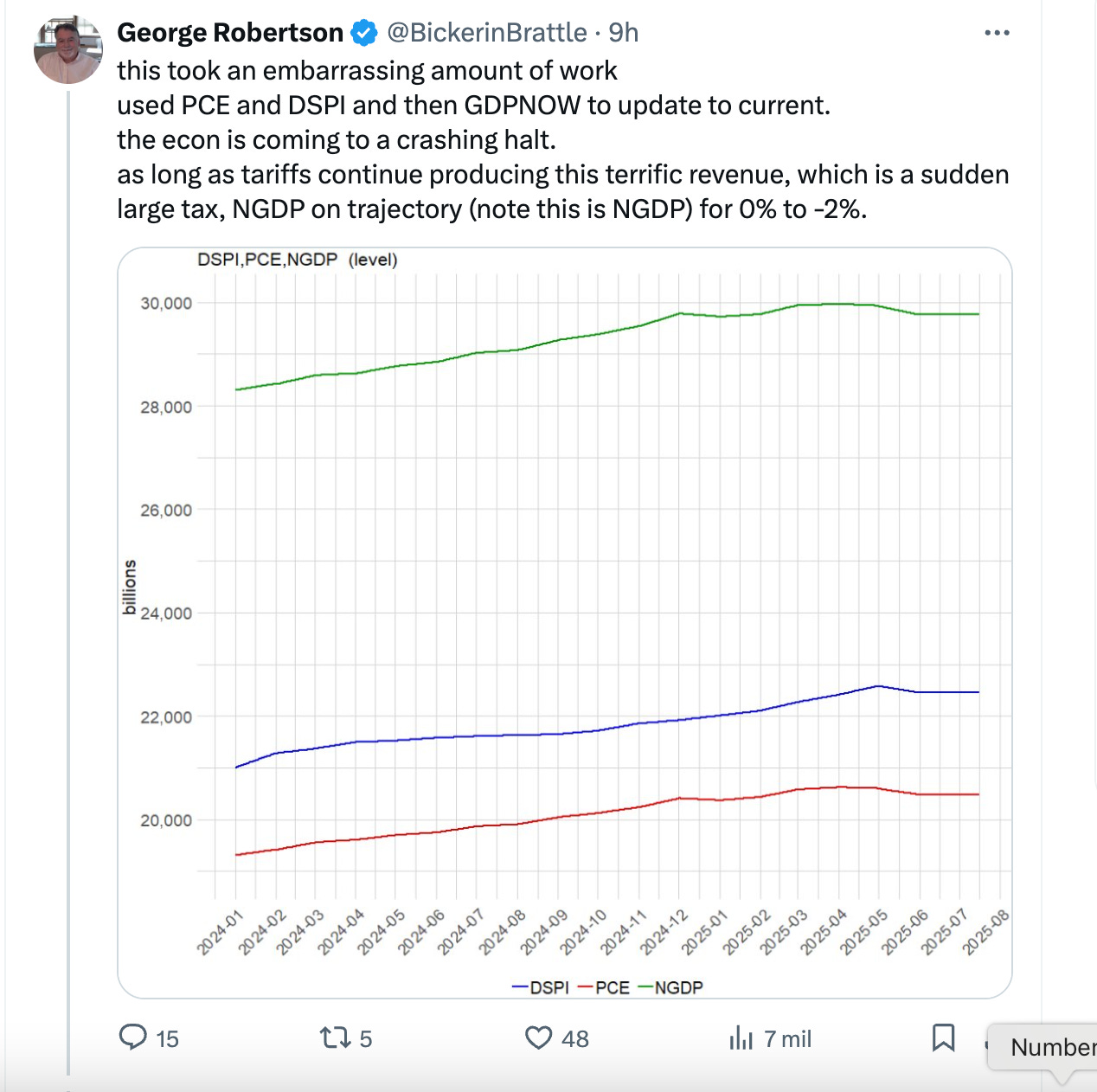

If this persists, we could see a significant hit to NGDP. George Robertson, from @themonetaryfrontier is being quite vocal on these concerns.

Again, this is a very big if, but let’s assume tariffs do persist and this impulse is taken away from the economy.

The Fed Will Make Another Mistake

The rate of change matters more than the level, and the direction is wrong. Fed Chair Powell knows this. Odds of a September rate cut have fallen to just 52%, down from near-certainty weeks ago.

The Fed is now afraid of rising inflation, making a rate cut less likely. However, if tariffs persist, then it will indeed be a lot more necessary to cut rates, as the economy could even enter a recession.

The Fed risks being late once again.

Pragmatic Investor Takeaway

Trump’s tariff shock isn’t just noise—it’s a policy shift that markets are ignoring at their peril. The immediate effect is inflationary: core CPI is already ticking higher, and August’s increases will push prices further.

The Fed is trapped—too hawkish and they crush growth; too dovish and inflation reignites. That’s the setup for a stagflation-lite scenario: higher prices now, weaker growth later.

So, what should investors look to buy now?

How are we repositioning our Macro Portfolio?

What will be the signs that a recession is coming?

Keep reading with a 7-day free trial

Subscribe to The Pragmatic Investor to keep reading this post and get 7 days of free access to the full post archives.