The Tesla Of Telehealth

Summary

A rapidly expanding telehealth company with a large and growing target addressable market.

The company generates most of its revenue from subscriptions and has seen significant growth (+50%) in subscribers and revenue.

The company sizable health dataset and leveraging AI, positioning itself as a leader in the telehealth industry.

My DCF model suggests an undervaluation of 30%, while my Elliott Wave analysis implies a potential return of 8x.

Overview

This is a rapidly expanding telehealth company growing at a fast click and quickly increasing profitability. It has a large and growing TAM and an attractive subscription-based business model.

The stock has had a good run-up since striking a low, but the price is still very compelling from both a technical and fundamental perspective.

I see this company as the “Tesla of telehealth”, as its great branding has made health "cool", just like Tesla did with EVs.

What does HIMS do?

HIMS can be broadly categorized as a telehealth company. Anyone who has seen their adverts on TV will have a better grasp of what the company does.

HIMS provides healthcare and healthcare-related products directly to consumers. You can go through their website and get connected with doctors who can prescribe medications, which they will send you on a regular basis.

Some of the most popular “treatments”/products include medication for hair loss, ED, weight loss or mental health. The company’s initial focus and main clientele, for the time, is men.

It’s a simple enough concept, and not necessarily something novel but there is a lot to like about HIMS.

First off, they address a very real and growing demand for male health products. The problem is men hate going to the doctor, right? HIMS solves this problem in two ways:

Creates a frictionless path to get the consumers/patient what he needs.

Re-frames health and going to the doctor into “self-improvement” and “wellness”.

Now, that’s for sure something we can all get behind. Who wouldn’t want to become a better version of themselves?

For consumers, HIMS solves a real problem in an efficient way. I’m not surprised they are growing so fast.

For investors, this is a great business model with recurring revenues, high markings and a large and growing addressable market.

Revenue and Profitability

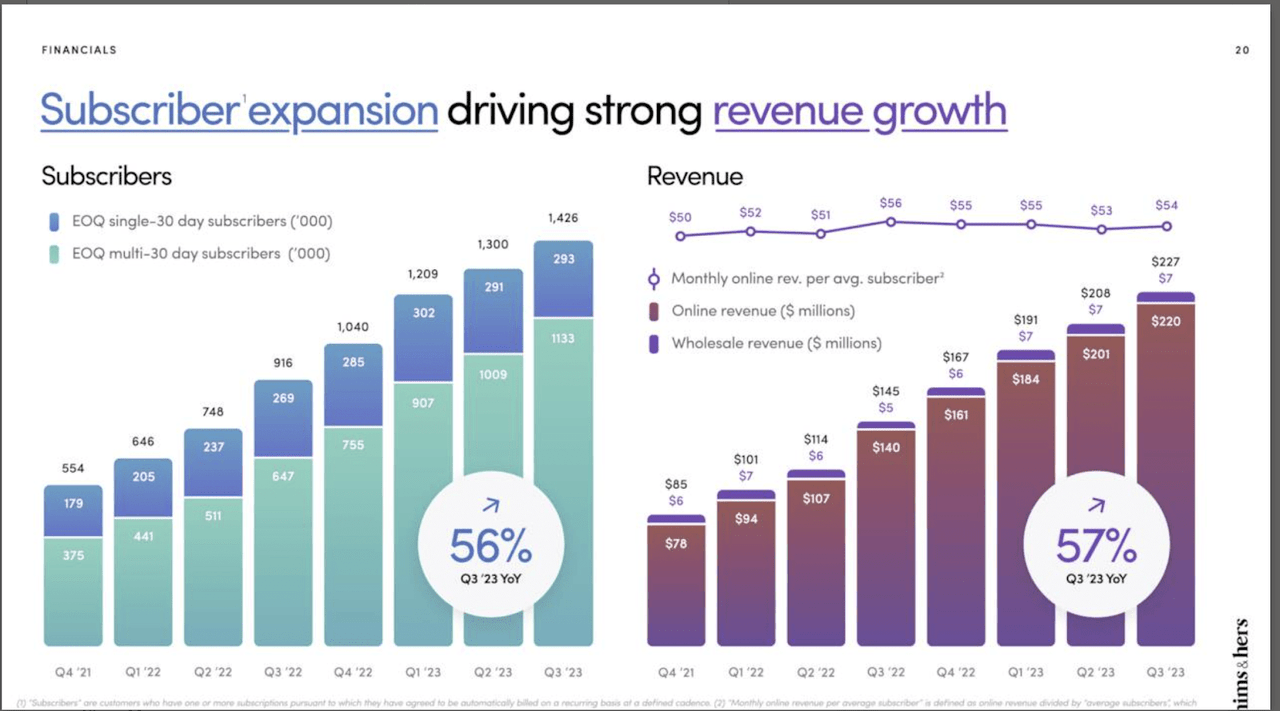

HIMS makes most of its revenues from subscriptions. Subscribe once, and you get products shipped to you monthly. Obviously, the business lends itself very well to this model. Once you begin a protocol/treatment, you are likely to remain on it for some time, perhaps even for life, and the subscription solves another problem.

Over 90% of the company’s revenues come from these subscriptions.

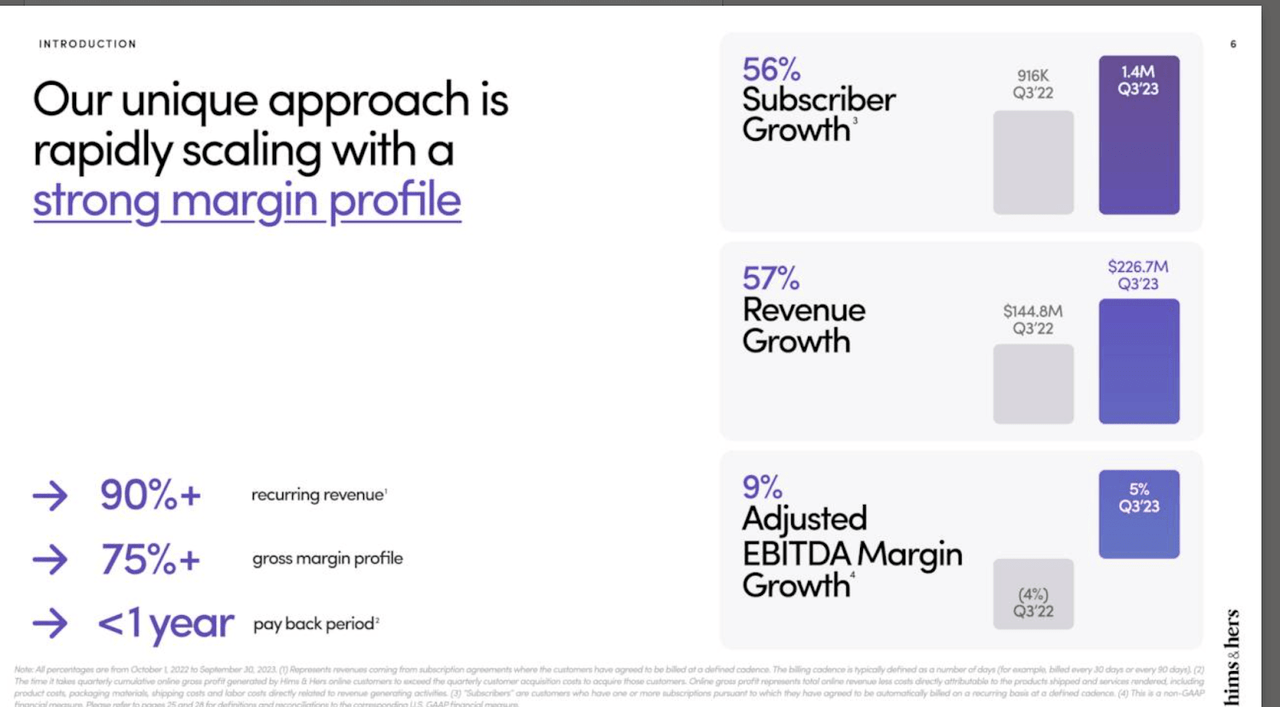

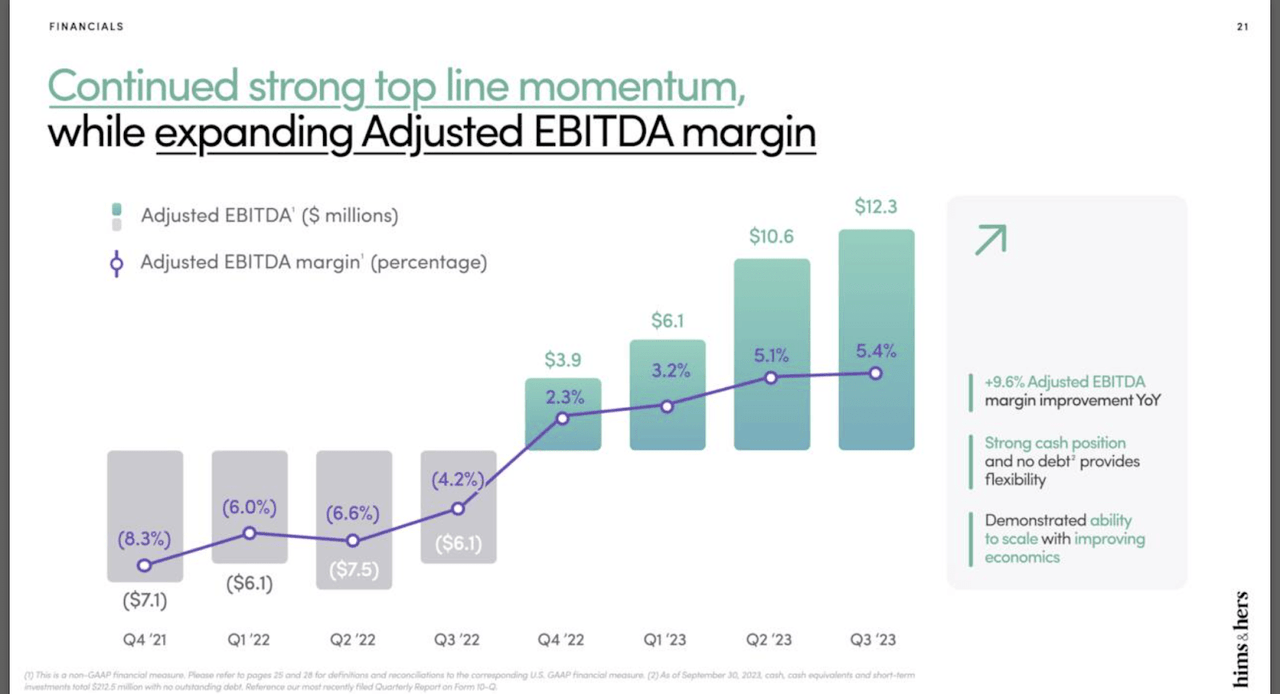

As we can see from the latest quarterly presentation, the company saw 56% subscriber and 57$ revenue growth, with a 75% gross margin and a notable increase from negative to positive adjusted EBITDA.

The key with a company like HIMS is to understand their Customer Acquisition Costs and Customer Lifetime Value.

There’s a price to acquire a customer and the value they bring to the company over their lifetime. If the latter is higher, it's obviously great.

Estimates indicate a CLTV of $350, significantly surpassing industry standards. On the other hand, the estimated CAC is $200, indicating a healthy return on investment. Indeed, the fact that Hims & Hers boasts a CLTV of $350, significantly surpassing their estimated CAC of $200, highlights a crucial financial advantage for the company.

Source: LinkedIn Report

While the company still reported negative EPS in the last quarter, profitability is increasing, and we know the company can generate substantial FCF. When a company is growing over 50%, though, you want them to spend aggressively.

TAM and Future Outlook

Now, let’s look at their Target Addressable Market:

According to the company’s report, this is what we could be looking at:

Hair Loss: $3B

Sexual Wellness: $4B

Mental Health: $14B

Dermatology: $44B

Total: $65B

These are huge growth areas, and this company is very well-positioned. They have already done very well addressing male issues, and they will be able to unlock even more growth if they can get into the female population and also become a larger player in mental health.

The potential for cross-selling and expansion is huge here.

And, of course, we can’t end this sections without talking about AI. The company announced an interesting new project in the latest earnings call.

It also announced the launch of a new AI-enabled offering currently in beta testing dubbed MedMatch, which provides healthcare providers with anonymized data points generated from the company's customer database to help identify suitable treatments for patients suffering from anxiety and depression according to their individual needs.

Source: mobilehealthenews

HIMS is building a huge medical database. What is the value of this data? Incalculable with the coming innovations in AI.

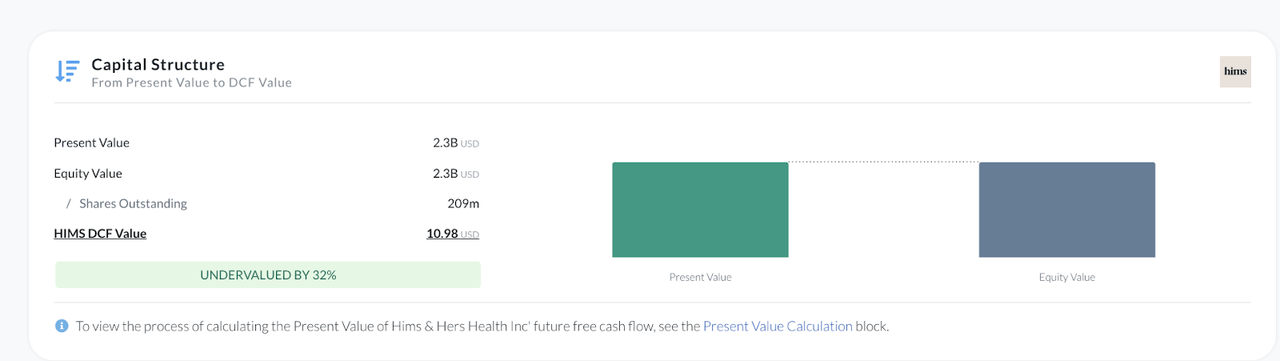

Valuation

HIMS is already turning into a potential cash cow, and inventors have begun to notice.

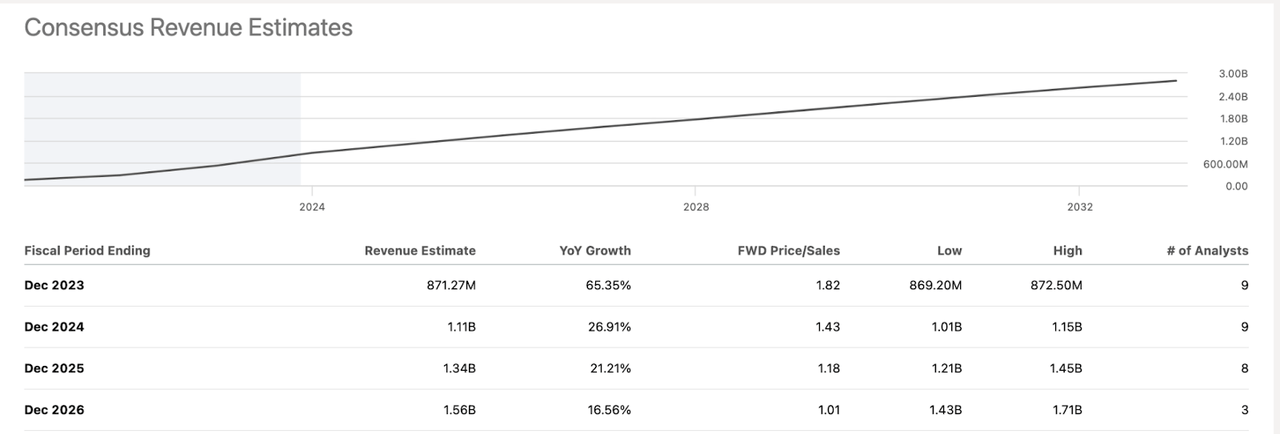

The company expects to hit around $870 million for 2023, with a 5% EBITDA margin. But this may only be the beginning.

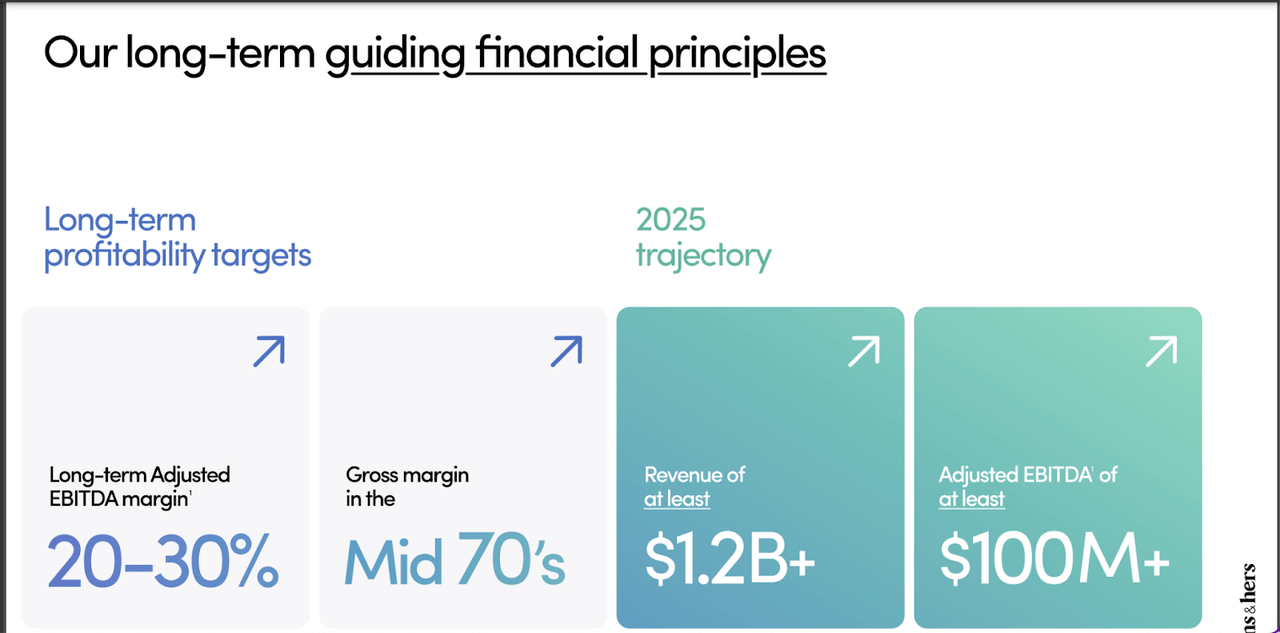

HIMS expects long-term adjusted EBITDA margin of 20%-30%, and over 1.2 billion in revenues by 2025.

Now let’s see what analysts think:

EPS will turn positive by 2025 according to analysts, with revenues going to $1.3 billion.

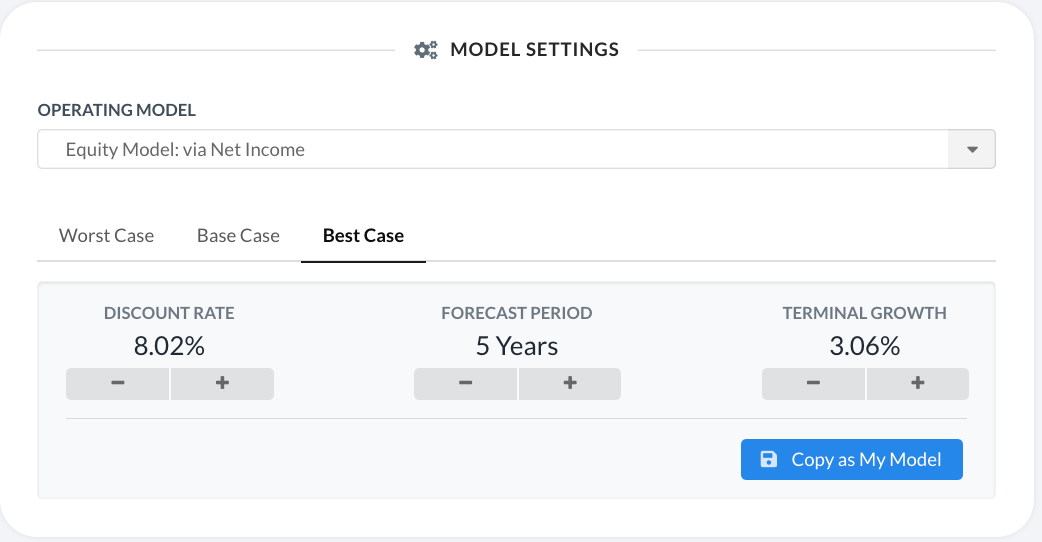

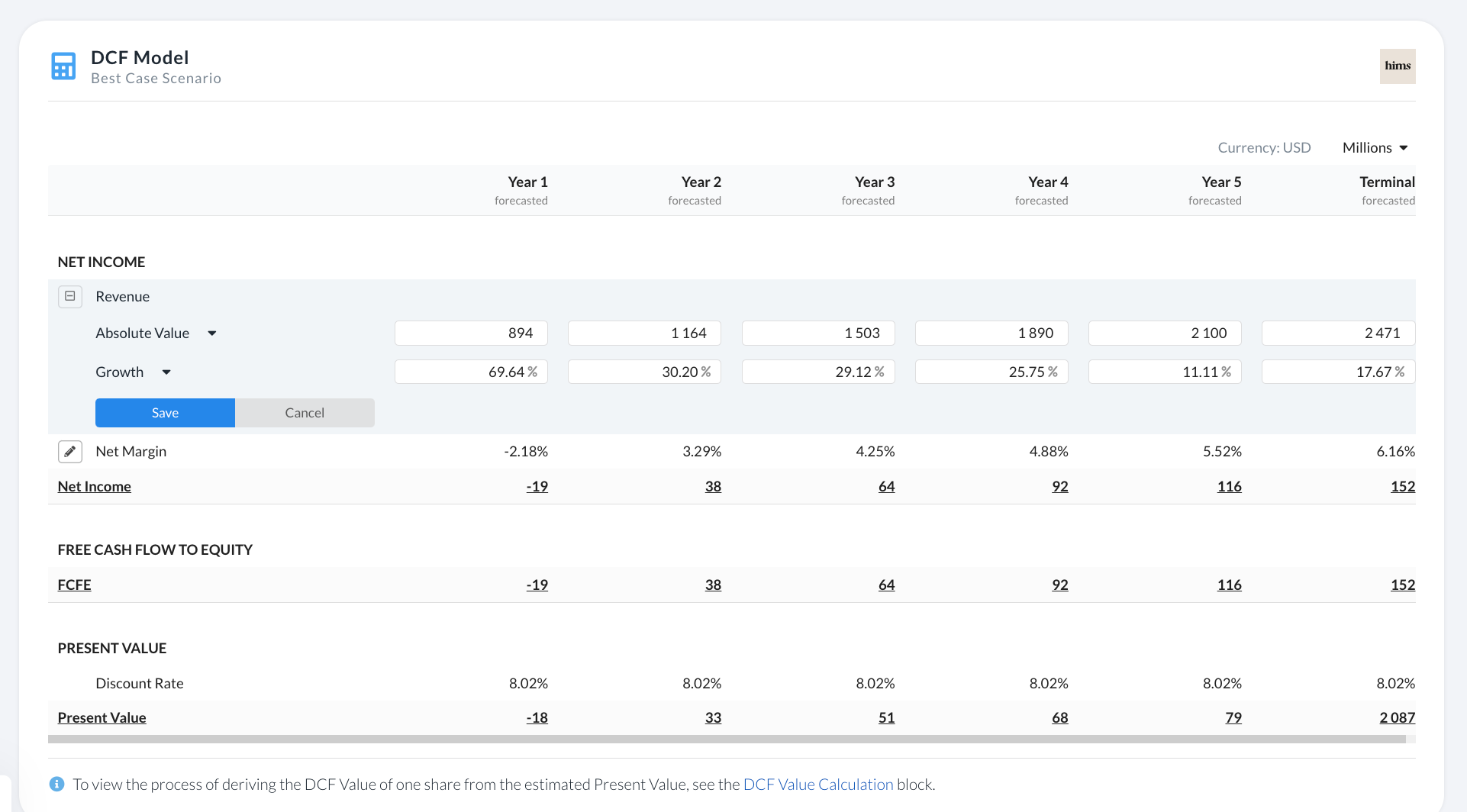

According to my DCF valuation, HIMS could be around 40% undervalued

:

This model uses a discount of 8.02%, with a terminal growth rate of 3.06%, and assumes net margins can grow to around 6.1%.

Another way of valuing the company would be looking at its PS, which currently stands at 1.92. Assuming the company continues to trade at a similar P/S, the stock price should be able to double by 2025.

If anything, with growing profitability, and as long as growth doesn’t slow down too dramatically, HIMS could easily experience multiple expansions.

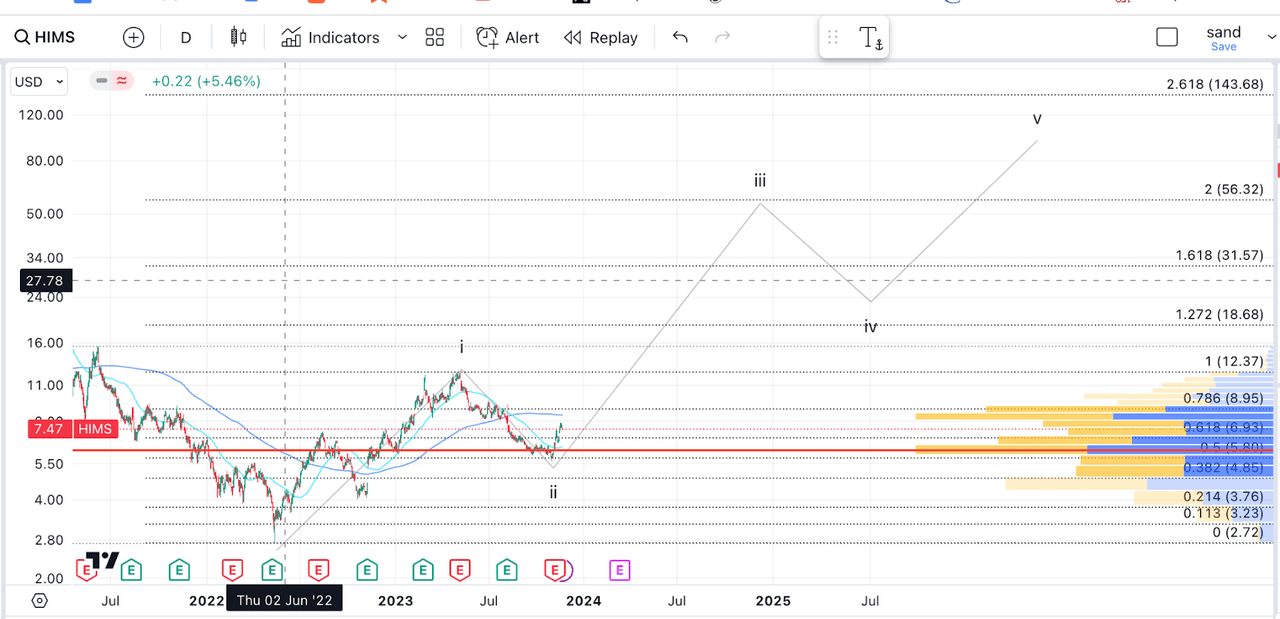

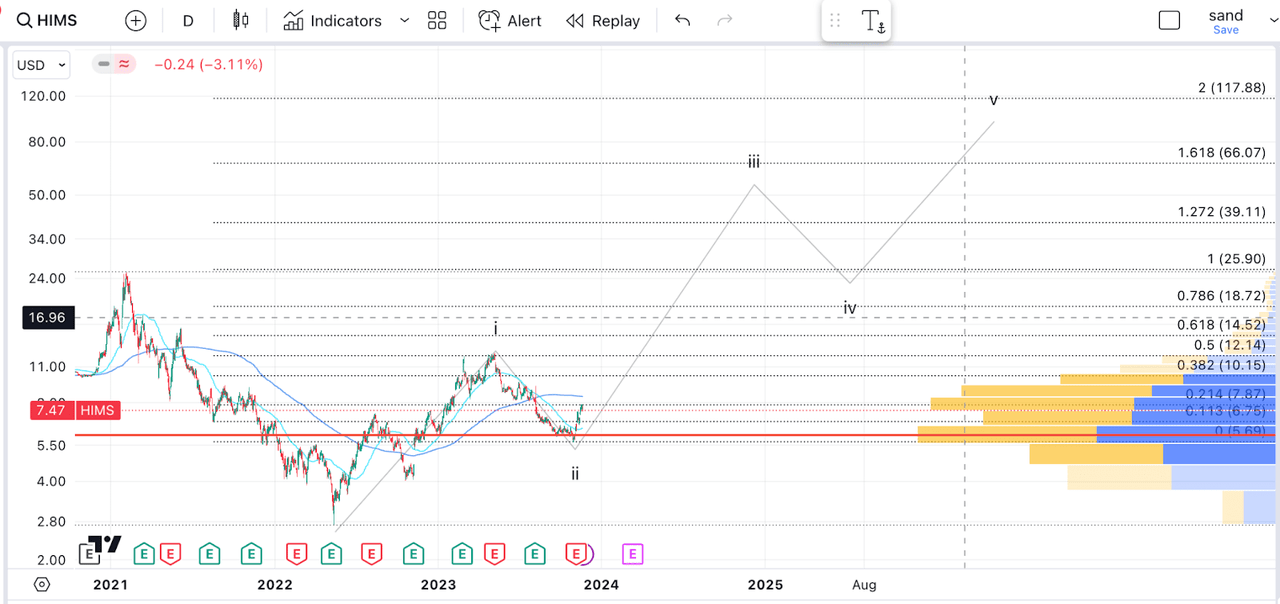

Technical Analysis

Looking at the technical chart, this is a reasonable place to add:

After reaching a bottom at $2.8, the stock has now staged a convincing rally, followed by a retracement to the 50% level, where we also have significant volume support.

And we have since rallied impulsively over 30%. In the short term, we could see a retracement before another big leg up. Notice we now have strong resistance above provided by the 200-day MA.

Taking the length of wave i from the bottom of our wave ii projects us all the way up to $66. This may seem very optimistic now, but remember HIMS was trading at over $25 at one point.

This is an exciting company, and I believe it could build up significant hype around it with a couple more solid quarters.

Takeaway

HIMS is incredibly promising, and sentiment has clearly shifted on this one. I think this company could do very well in the coming decade, as it leverages the best of healthcare and technology. I am going to be starting a position here and looking to double down if we can retrace further from here.